Market research firm Wood Mackenzie has predicted that the US energy storage market will almost quadruple over the next six years.

Wood Mackenzie released its Q2 2026 US Energy Storage Monitor report on 23 June, which said the US energy storage market would reach 200GW/655GWh of cumulative installed energy storage capacity by 2031.

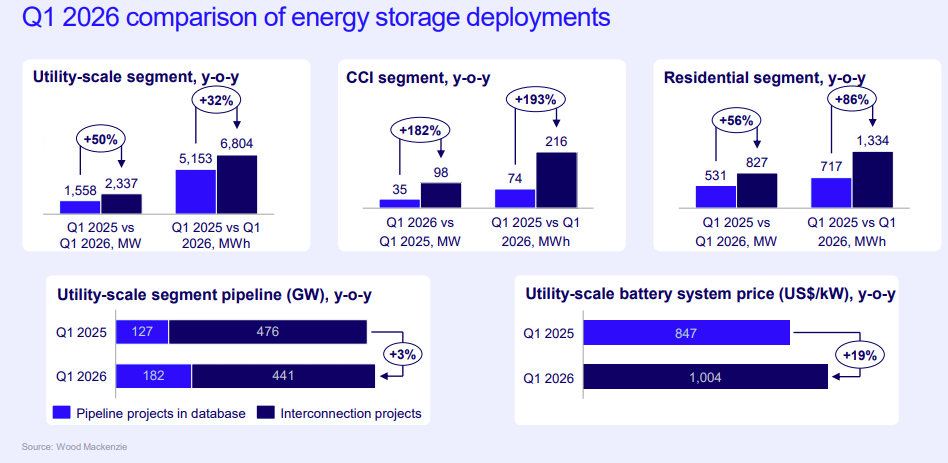

According to the report, 3.3GW/8.4GWh of energy storage was installed in Q1 2026, with all segments posting record Q1 installation numbers.

The utility-scale sector deployed more than 2.3GW/6.8GWh in Q1 2026, reflecting project carryover from 2025 as developers prioritised safe-harbouring activities in the second half of last year.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Commercial and industrial (C&I) installations reached 97.7MW in Q1 2026, a 27% quarter-over-quarter increase, with California accounting for 75MW. Residential storage achieved a record 1.3GWh in Q1 2026, up 86% year-over-year and 5% quarter-over-quarter, driven by a surge of installations completed in late 2025 ahead of the Section 25D tax credit expiration.

Utility-scale

Texas, California, and Arizona continued to lead Q1 2026 deployments, while emerging markets with vertically integrated utilities—particularly Michigan and Georgia—showed increasing momentum.

Looking ahead, Wood Mackenzie forecasts utility-scale storage will expand at a 7% average annual growth rate (AAGR), with acceleration expected between 2028 and 2031.

Near-term market growth will be constrained by safe-harboured capacity and limited availability of foreign entity of concern (FEOC)-compliant BESS systems. As domestic battery cell manufacturing scales up, however, the segment is positioned to address rising electricity demand, compensate for thermal generation retirements, and support renewable energy integration.

While Texas and California are expected to remain key markets over the forecast period, emerging markets, such as New York and Illinois, will see higher growth.

C&I segment

California led the market with a record 74MW of C&I installations, and the state is expected to sustain this growth trajectory through 2026 supported by incentive programmes including the Net Billing Tariff (NBT) and Self-Generation Incentive Programme (SGIP).

Meanwhile, Illinois, Maryland, Massachusetts, and New York are all positioned for continued expansion in the community storage market, with a combined project pipeline exceeding 215MW.

Annual C&I storage installations are projected to grow 27% from 2026 to 2031.

California’s robust Q1 2026 performance is expected to sustain momentum in the C&I segment through the end of the decade, with continued access to the investment tax credit (ITC) driving greater adoption of both retrofitted and standalone storage systems as solar developers expand their portfolios into energy storage. Growth is anticipated in both the near and long term for community storage,

Residential storage

The national attachment rate reached 45% in Q1 2026, up from 38% in Q1 2025 and unchanged from 45% in Q4 2025. California, Texas, Hawaii, and Arizona experienced the largest quarter-over-quarter increases in storage capacity deployed during the first quarter.

Looking ahead, the national residential storage market is projected to contract 5% in 2026. US residential solar installer Freedom Forever’s bankruptcy, constraints in tax equity availability, and updated permitting data all contribute to expectations of a sharper decline in capacity additions.

Wood Mackenzie’s latest report aligns with its previous US Energy Storage Monitor for Q1 2026, which forecast that the US energy storage industry will install around half a terawatt-hour of new capacity over the next five years.

The firm also withdrew its expectation of a near-term market contraction, as a record number of projects commenced construction in late 2025 to secure the ITC, offsetting the shortfall from reduced activity during the middle of the year.