Operating battery energy storage systems (BESS) in the UK will need to use “more complex trading strategies” to turn a profit in the saturated UK BESS market, according to BloombergNEF researcher Sonia Grunenwald.

Grunenwald spoke yesterday afternoon on the first day of the Renewables Procurement & Revenue Summit, held by Energy-Storage.news publisher Solar Media. During a presentation on revenue stack options for battery developers in the UK, Grunenwald first highlighted NESO’s shift from a “first come, first connected system” to a “first ready, first connected” system that has discouraged speculative applications for grid connections, and freed up much space in the UK’s grid queue.

“In effect that really clogged the grid connection,” explained Grunenwald. “NESO started clearing out the queues and 153GW of storage was dropped from the existing 240GW queue; that’s enormous.”

Grunenwald added that these commissioning delays have impacted the profitability of many batteries, as they are waiting in grid connection queues rather than operating and generating revenue.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

“It’s a global issue, but it’s been very predominant in Europe, in countries like Germany, Italy and the UK; we’ve seen very large grid connection queues, where a large portion of the queues are made up of storage projects,” she explained. “This directly eats into your project margins as your project is sitting there idle until it’s actually able to get connected.”

The diminishing of these delays, alongside a 31% year-on-year decline in turnkey BESS costs, means that developers may be financially incentivised to deploy batteries in the UK at present.

UK reaches BESS saturation

However, Grunenwald noted that the remaining connection queue backlog still exceeds the total volume of batteries that BloombergNEF expects to come online in the next decade, saying: “there’s still about 90GW that’s prioritised by 2035 [which is] still above what we expect to come online by that point.”

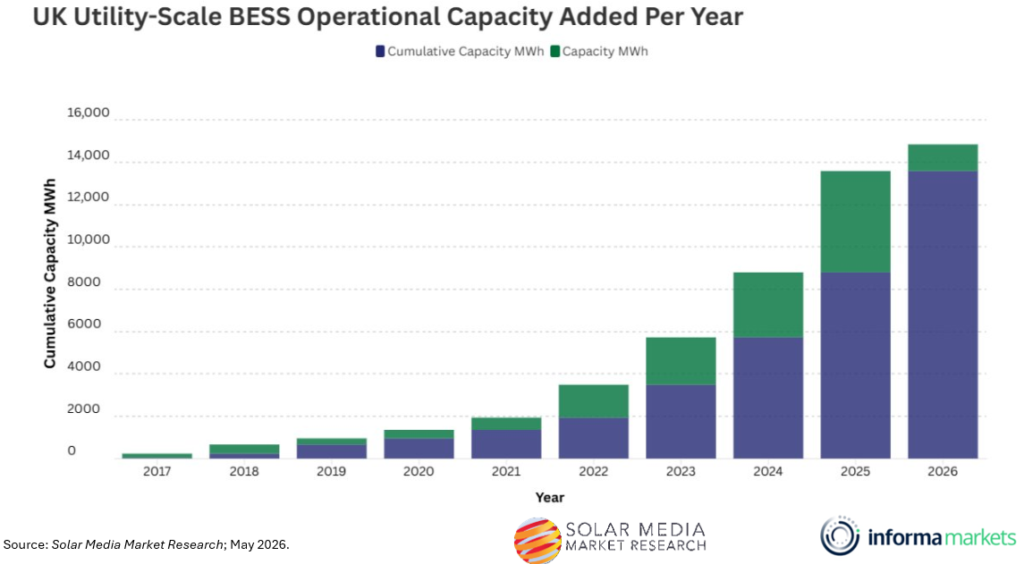

The batteries that do come online will also have to contend with complex market dynamics that require a similarly complicated revenue stack in order to turn a profit, not least because of the popularity of deploying new batteries in recent years; figures from Solar Media Market Research show that new utility-scale BESS capacity added in the UK has increased each year since 2017, as shown in the graph below.

Grunenwald says that operators of newer projects will have to develop more complex financial mechanisms for their projects.

“A battery cannot really rely on charging during the two lowest-priced hours and then discharging at the two highest-priced hours, and do that day-in, day-out, and expect to break even,” she explained. “That doesn’t work in the UK. However, it doesn’t mean that a battery cannot make economic sense in the country, or else we wouldn’t see that many installations.”

“That’s when we start seeing much more complex trading strategies and aggregation strategies come together,” Grunenwald continued. “When speaking with developers, a lot of these strategies start with aggregating a bunch of different batteries into a portfolio, and starting to trade both in the day-ahead and intraday market, to try to optimise dispatch over that time, reduce how many cycles you’re going to be able to do and, at the end of the day, maximise revenue across the entire portfolio.”

This article has been amended from its original form to correct a data reporting error pertaining to the UK’s cumulative battery storage installations.

Solar Power Portal publisher Solar Media is hosting the Renewables Procurement & Revenue Summit, this week in London. The event will cover PPA design, tackling high energy prices and more; for more information, including the full agenda and ticket options, visit the event website.