Managers of the UK’s largest BESS owner-operator Gresham House Energy Storage Fund (GRID) discussed recent investment news and future strategy this week.

GRID is listed on the London Stock Exchange and is run by asset manager Gresham House. The company explained a new investment partnership with a Sumitomo Corporation-controlled entity and set out its long-term strategy in a capital markets day presentation yesterday (28 May).

Like other UK-listed battery energy storage system (BESS) funds, its value plummeted over the course of 2023 and early 2024 as revenues in the UK fell, and has not recovered since. Ben Guest, manager of the fund which has over 1GW online in the UK, said the valuation does not reflect its potential.

“We think we’re a growth company, but not valued as one,” he said in the presentation.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Equity financing partnership with Summit Transition Partners

Funds like GRID helped kickstart the UK grid-scale energy storage market by raising capital through listing publicly and putting that money into BESS projects, alongside debt project finance. However, since the fall in share prices, raising that capital is much harder. However, since the fall in share prices, raising that private capital is much harder.

The company has now opted for a different approach, bringing on Summit Transition Partners (STP) as an equity investment partner. STP is controlled by Japanese conglomerate and trading house Sumitomo Corporation with participation from TPK Holding. It will cover the bulk of the equity investment needed for five projects totalling 697MW, starting with three totalling 397MW, with debt covering the rest.

“Bringing in outside capital reduces our required equity significantly,” Guest explained. “It reduces our EBITDA, but means a much smaller level of capital required so de-risks our business.”

“It crystallises some of the value we’ve created on our projects, reduces day one capital requirement from GRID and boosts our equity returns,” added James Bustin, assistant fund manager for GRID.

“It’s a funding structure for the first three projects which also creates a framework for the future pipeline.”

Revenue development

A key part of the fall in UK BESS revenues in 2023/24 was a lack of take-up in the balancing mechanism (BM), which the industry had hoped would help offset anticipated falls in ancillary service prices. Utilisation of BESS in the BM was very low in that period and, while it is improving, is still not where BESS operators say it should be. This lack of the full utilisation of BESS is a problem cited by the industry in many other markets too.

“We have not yet demonstrated GRID’s full revenue potential and will now look to do that,” Guest said.

On the BM, he said that the next month should see a transformation in utilisation as the UK’s National Energy System Operator (NESO) control room brings in new capabilities and software.

A big change will be the ability to immediately see the state of charge (SOC) of every BESS on its network. It currently cannot see this, making operators more reluctant to dispatch BESS in the BM instead of conventional gas generation.

Guest also pointed out that, more broadly, the gas sector should decline since no new gas capacity was awarded contracts in the most recent capacity market (CM) T-4 (existing operational gas projects were).

But more generally, Guest said that the company sees a need to diversify its revenue away from NESO. An untapped, potentially large area could be long-term trading, something he explained in detail on the call.

Essentially, this is committing to sell power over longer periods in larger volumes to buyers than it currently does (typically day-to-day trading). Interestingly, the success of this strategy is inversely correlated to the success of day-to-day trading. That is because day-to-day trading capitalises on price spreads, whereas long-term trading is about managing the risk of those price spreads for clients (so benefitting if those spreads are low).

This thinking sounds similar to the untapped potential for BESS in ‘long-term optimisation’ posited by Sweden-based optimiser and VPP firm Flower.

Augmentation and 8-hour BESS

Alongside the new projects, the company is going big on augmenting its existing ones. By the end of 2026 its 1GW+ UK portfolio will on average be around 2-hours. In 2024, Bustin said that an initial California market entry was cancelled because it made more sense to use that money to augment its UK ones.

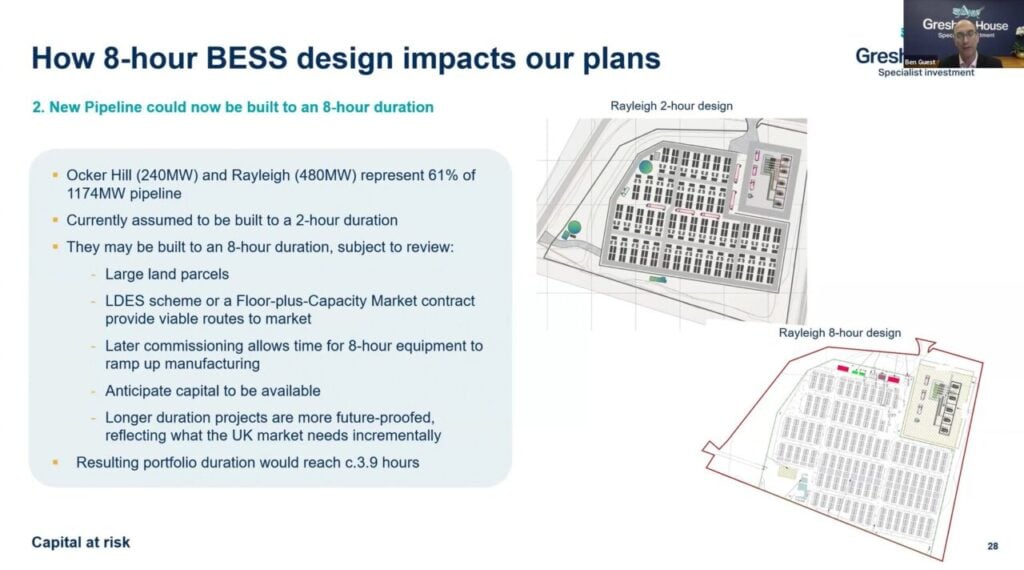

But, even more interestingly, the company went into a lot of detail on the potential of 8-hour BESS. That is far, far longer than any project is being deployed at today in the UK, which is at most 3- to 4-hours.

The company didn’t give a timeline on when it might deploy an 8-hour project, but said its recently acquired Ocker Hill (240MW) and Rayleigh (480MW) could be built to 8-hours instead of the 2-hours currently planned. It sounds like their power capacity would be reduced to do so, however, so Rayleigh wouldn’t necessarily be a 3.8GWh project.

An 8-hour project would help with trading capture power price spreads for longer. And there are various routes to market for such a large project, including the CM, floors and tolls and the UK government’s long-duration energy storage (LDES) cap and floor. The firm has moved to have around 50% of its portfolio’s revenues secured through tolls or floors.

Guest also said that 8-hour systems are much cheaper relative to capacity than 2-hour ones, as the gentler cycling reduces the need for any cooling systems and increases round-trip efficiency (RTE) and cycle life.

8-hour systems have always been possible simply by reducing a system’s power output, but systems designed specifically for 8-hour duration are a relatively new thing. Industry veteran Marek Kubik discussed this trend, driven by long-duration battery cells, in a recent video interview.

Sale and de-listing of GRID?

In the Q&A section of the presentation, someone in the audience asked a direct question on the future of the fund: how long do its managers wait before conceding they are not delivering value and pursue alternative avenues?

While not naming it, this was clearly alluding to one option of selling the fund to private investors, as Harmony Energy did with the Harmony Energy Income Trust (HEIT) fund. The questioner asked what they would do if a large industrial came in to make an offer on GRID.

John Leggate, chairman of the GRID board, responded: “We have a runway to let these plans feed in. Over the course of the next year, if we’re not getting results then we have the obligation to consider alternatives. Right now we are focused on these plans but at some point we will certainly review their progress.”

“You can never tell with these things and I would rather not speculate on what might happen, we’ll keep our heads down. These events are to put information out into the market. If anyone is interested, just look at our data. If someone shows up with something interesting, the board will take it seriously.”