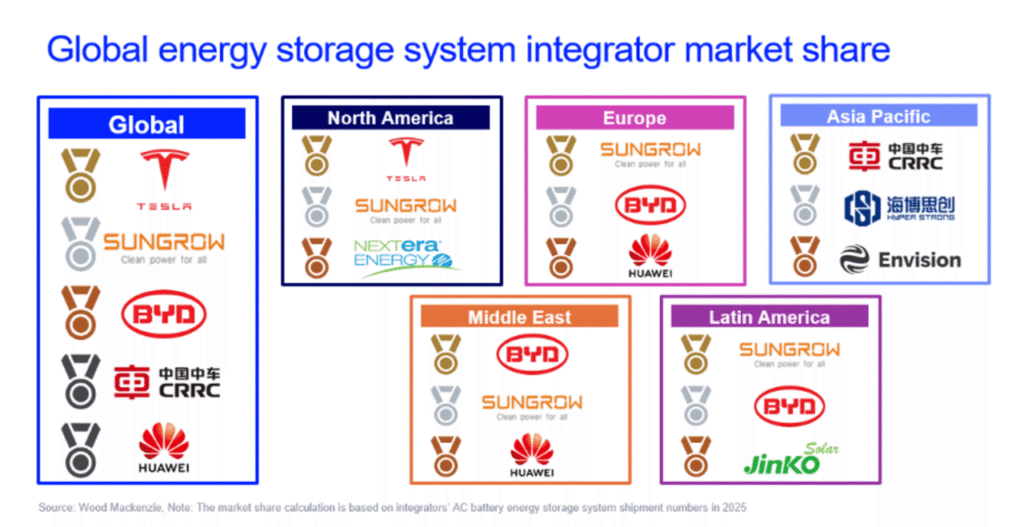

Chinese system integrators have cemented their dominance of the global battery energy storage system (BESS) market, capturing 76% of global market share in 2025.

According to market research firm Wood Mackenzie’s “Global energy storage system integrator market share 2026” report, eight of the top 10 global system integrators are headquartered in China.

Tesla and Sungrow retained the top two positions for the third consecutive year, while BYD advanced five places to claim third, as the market installed over 320GWh of capacity, a year-over-year increase of more than 50%.

System integrators design, assemble, and deliver complete BESS solutions, distinguishing them from cell manufacturers who supply battery components.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

China’s CATL, the world’s largest BESS cell manufacturer with 121GWh shipped in 2025, does not appear in Wood Mackenzie’s integrator rankings because it operates primarily as a cell supplier rather than delivering turnkey systems.

The integrator market is more fragmented than cell manufacturing. The top 10 system integrators captured approximately 68% of the market in 2025, with the remaining 32% split among Tier 2 and Tier 3 players, up from just 18% in 2024.

Regional dynamics

In North America, Tesla retained its leadership position, supported by its Megapack hardware, Autobidder software, and US-based manufacturing. NextEra Energy entered the top three for the first time, benefiting from its vertically integrated position.

The competitive landscape faces imminent transformation through new federal legislation. The “One Big Beautiful Bill Act” (OBBBA) establishes escalating domestic content requirements for projects seeking federal tax incentives, beginning at 55% in 2026 and reaching 75% by decade’s end. These thresholds create substantial barriers for Chinese suppliers.

Sungrow leads the European market, with BYD and Huawei rounding out the top three—an entirely Chinese podium. Geographic expansion is accelerating beyond traditional strongholds in the UK, Germany, and Italy, with six additional countries now forming a substantial secondary market tier.

Policy pressure is intensifying through the Net Zero Industry Act (NZIA), the Industrial Accelerator Act (IAA), and the EU Batteries Regulation, all designed to reduce European dependence on Chinese supply chains.

Notably, BESS solutions became Sungrow’s largest revenue segment in 2025, at 42%, surpassing its PV inverter business (36%), a significant milestone for a company built on solar PV inverter technology.

In APAC, CRRC secured the regional top position for a third year, with HyperStrong and Envision following. China’s domestic market represents approximately 85% of Asia-Pacific volume, giving local integrators an overwhelming home-field advantage.

Southeast Asian markets are emerging as a next growth frontier, with five countries advancing regulatory frameworks to support utility-scale storage deployment. Australia stands apart as the region’s most competitive market for Western integrators, where stringent technical requirements and financing preferences create opportunities for non-Chinese firms.

The Middle East entered “an era of mega-scale procurement”, with the UAE announcing a 5.2GW solar project paired with 19GWh of storage, and Saudi Arabia’s tender rounds covering 5GW/20GWh. BYD and Sungrow together captured 87% of the regional market.

In Latin America, Chile leads with the most mature regulatory framework, with BYD’s contracted volume with Grenergy reaching 6.5GWh across the Oasis de Atacama project.

BYD’s rise to third place in Wood Mackenzie’s rankings reflects the competitive advantage of vertical integration. As both a leading cell manufacturer (10% global cell market share) and system integrator, BYD controls more of its supply chain than competitors, providing cost advantages and supply chain security.

“Competition in the global BESS integrator market is shifting from scale alone to a multidimensional set of capabilities,” said Jiayue Zheng, senior research analyst at Wood Mackenzie.

Zheng continued, “Policy compliance, grid-forming technology, software-driven revenue optimisation, and financing support are becoming decisive competitive variables. Integrators that can meet these demands across diverse regulatory environments will build the most durable market positions through the remainder of the decade.”

Grid-forming inverter technology, sophisticated software platforms like Tesla’s Autobidder, and project financing capabilities are increasingly differentiating winners from the rest of the pack.