Battery energy storage systems (BESS) in Australia’s National Electricity Market (NEM) more than tripled their daytime-to-evening energy shifting in the first quarter of 2026, according to AEMO’s latest Quarterly Energy Dynamics report.

Average battery discharge reached 359MW during the quarter, more than three times the 98MW recorded in the same period a year earlier.

This growth was driven by 4,445MW of new large-scale battery storage systems, adding 11,219MWh to the grid since the end of Q1 2025, more than doubling total installed battery storage in the NEM.

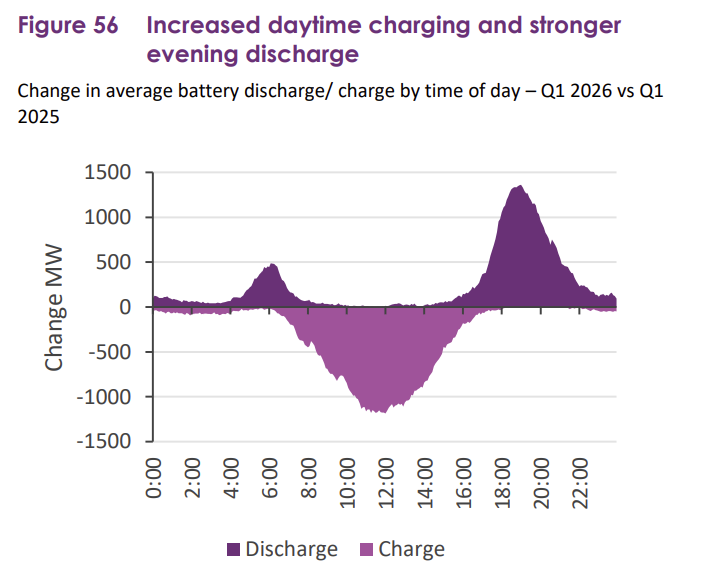

Daytime charging increased by 872MW, while evening peak discharge rose by 818MW, shifting energy from daylight hours into periods of higher demand. Battery storage delivered 1,115MW into the evening peak, with peak discharge reaching a record 3,556MW on 7 January during the half-hour ending 19:00, 23% higher than the previous record set in Q4 2025.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Eight battery storage systems commenced commissioning in the NEM during Q1 2026, including the 415MW/1,660MWh Orana BESS in New South Wales, the 300MW/650MWh Mortlake BESS in Victoria and the 260MW/1,090MWh Supernode BESS unit 2 in Queensland.

Total installed battery storage systems, including commissioned and commissioning assets, exceeded 8,000MW by the end of the quarter.

Price-setting role expands as arbitrage revenues climb

Battery storage set prices in 32% of trading intervals across the NEM during the quarter, displacing hydro as the most frequent price-setting technology.

The increased battery capacity contributed to lower year-on-year wholesale prices in most regions, with the NEM average wholesale spot price averaging AU$73/MWh (US$51.97/MWh, down 12% from Q1 2025.

Evening peak prices fell as battery discharge reduced reliance on gas and hydro generation, though this effect was moderated by an increase in daytime prices as battery charging set prices more frequently, reducing the frequency of negative prices in the northern regions.

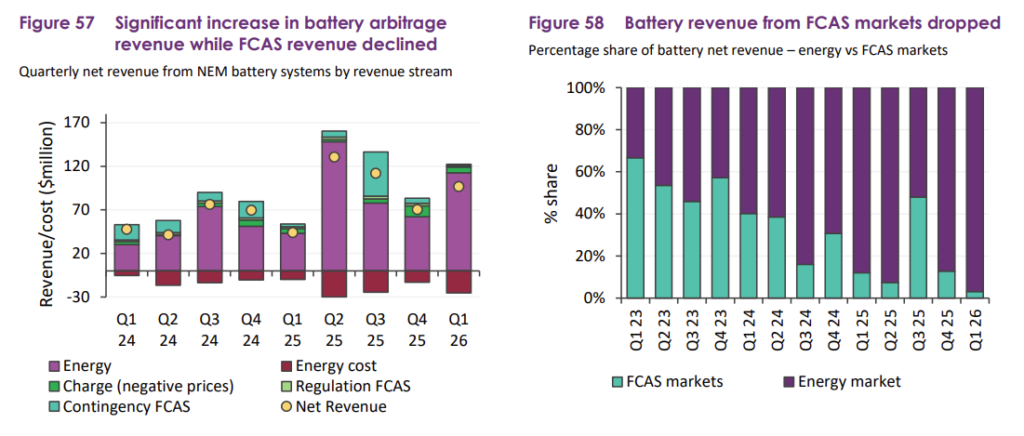

Estimated revenue for NEM grid-scale battery storage systems averaged AU$96.9 million, more than double the AU$44 million recorded in Q1 2025.

Energy arbitrage revenue rose by AU$55.1 million to AU$93.9 million, accounting for 97% of total battery storage revenue, up from 88% a year earlier. Frequency control ancillary services (FCAS) revenue declined to AU$3 million, down 43% from the previous year, representing just 3% of total revenue.

NEM-wide battery price spreads declined from AU$183/MWh in Q1 2025 to AU$121/MWh, reflecting lower spot price volatility.

Queensland and Victoria recorded the sharpest declines in average price spreads, falling 68% and 41% to AU$78/MWh and AU$86/MWh, respectively, while South Australia saw an increase to AU$328/MWh driven by volatility events.

The growth in battery storage systems comes as Australia’s BESS pipeline continues to expand.

Standalone battery storage in the NEM connections pipeline increased from 20.5GW in Q1 2025 to 33.2GW in Q1 2026, a 62% increase, with battery storage now comprising 49% of the total 67.3GW of projects progressing through the connection process.

Around 74% of battery storage projects in the pipeline feature grid-forming inverters, which can provide essential system services and help maintain grid stability as coal-fired generation continues to decline.

New South Wales has been warned that 75% of its 56GWh storage requirement for 2030 has not yet reached financial investment decision, with the state’s storage needs increasing from an earlier estimate of 40GWh due to higher-than-expected solar adoption.

“Two years ago, we needed 40GWh of storage operational by 2030. That has now increased to 56GWh solely due to solar penetration. Of the 56GWh needed, 12.5GWh has hit the financial investment decision. 75% of what we need in 2030 is not there today,” Paul Peters, CEO of New South Wales’ Energy Security Corporation, said at the Energy Storage Summit Australia 2026 last month.

Renewables supplied 46.5% of NEM generation during the quarter, the highest share on record for a first quarter, driven by increased wind and solar output.

Grid-scale solar output reached a new quarterly high of 2,706MW, up 13% from Q1 2025, while wind output increased 9.3% to average 3,845MW.

Coal-fired generation fell to a new Q1 low at 13,102MW, down 4.4% year-on-year, while gas-fired generation recorded its lowest average for any quarter since Q4 1999 at 712MW, 24% lower than in Q1 2025.

Peak renewable energy and storage contribution in the NEM reached 76.7% during the half-hour ending 11:30 on 7 January, 4.3% higher than the previous Q1 outcome. South Australia set a record for renewable energy generation and storage contribution, reaching 98.8% during the half-hour ending 15:00 on 31 January.

In Western Australia’s Wholesale Electricity Market (WEM), battery discharge increased by 108MW, driven by the commissioning of 1,025MW/4,100MWh of new battery storage systems since the end of Q1 2025. The renewable energy share of generation increased to 46.1%, up from 40.8% in Q1 2025.

Interested in Australia? Read Energy-Storage.news’ Energy Storage Summit Australia coverage and related content.