Energy-Storage.news Premium speaks with wholesale electricity policy expert, Andrew Levitt, and Dr Long Lam, managing energy associate at the Brattle Group, about PJM and managing load growth.

Consultancy firm, The Brattle Group, recently published “Impacts of Large Loads on Electricity Rates: A Primer,” a whitepaper prepared for the Energy Systems Integration Group (ESIG), and involving Dr Lam, an expert in the development and implementation of decarbonisation strategies.

Andrew Levitt is an expert in wholesale electricity policy, with a focus on evolving system needs, and was recently involved in Brattle’s assessment of PJM’s proposed transmission services for large loads, such as data centres, co-located with generation.

PJM Interconnection is grappling with unprecedented load growth projections and a capacity market design that stakeholders increasingly view as inadequate for the present moment.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

In January, the Trump administration, with a bipartisan group of governors, US Secretary of Energy Chris Wright, and Secretary of the Interior Doug Burgum, urged PJM to “temporarily overhaul its market rules to strengthen grid reliability and reduce electricity costs for American families and businesses by building more than US$15 billion of reliable baseload power generation.”

In a decision released later that month, PJM’s plan did have some overlap with the requests made by the officials. As part of its decision, PJM announced it would be initiating a “Reliability Backstop Procurement”.

PJM’s decision continued, “Over the longer term, the Board does not view it as desirable for PJM to serve as the procuring authority to long-term commitments resulting from backstop procurement. Accordingly, any such procurement should be viewed as a transitional measure intended to facilitate the timely integration of new supply, while options for a more durable mechanism are evaluated as part of the broader market review directed below.”

On 6 May, the grid operator released its whitepaper, “Powering Reliability Through Market Design,” laying out three distinct pathways for reform, each with different implications for how the nation’s largest wholesale electricity market will procure resources, manage costs, and integrate new technologies like battery energy storage systems (BESS).

At the heart of PJM’s challenge is the capacity market’s single clearing price mechanism, long considered a linchpin concept for restructured electricity markets, which is being challenged by political pressures that have capped prices below the cost of new entry.

This has created a situation where, as Levitt notes, “basically no new resources are in the money in PJM today, based on wholesale revenues.”

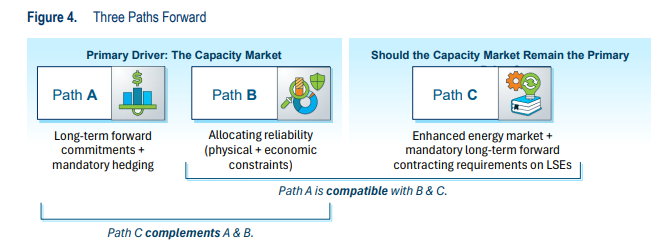

PJM’s three paths

PJM’s whitepaper presents three potential reform pathways, each representing a different philosophy about the role of markets versus state intervention in resource planning.

Path A: Stabilised Markets:

Path A would require longer-term hedges and commitments, bringing states more heavily into resource investment decisions. This approach would look somewhat similar to the centralised planning models used in California or New York, where regulators play a strong role in determining the resource mix.

Under this pathway, large load customers, such as hyperscalers and data centres, would likely face substantial financial commitments through large load tariffs, potentially requiring deposits or letters of credit worth billions of dollars to protect existing customers from stranded cost risks.

Path B: Differential Reliability:

Path B represents a mix-and-match approach that draws sharper lines between PJM’s responsibilities and state responsibilities. This pathway acknowledges that different states may make different choices about resource procurement, allowing for a variety of approaches across PJM’s 13-state footprint.

Path C: Energy Market Transition

Path C would maintain a lighter state touch, relying more heavily on market signals to drive efficient resource investment. This approach would look more like the Electric Reliability of Texas (ERCOT) market’s energy-only market design, with more precise price signals and better valuation of flexibility.

Under this model, incumbent customers could be protected through long-term hedges while large loads enter without such protections, potentially driving spot market prices higher without impacting residential customers.

“I think they’re all adequately suited to meeting load growth in different ways,” explains Levitt. “Some require more central administration of resource investment, so they’ll be heavier on the states. Others are a lighter touch, and there will be strong enough market signals that they can drive an efficient resource mix.”

Load growth

Driving much of this reform discussion is PJM’s sharp upward revision in load forecasts, primarily fueled by anticipated data centre development. The load forecast shows a large increase in expected demand over the next decade.

In October 2025, the US Energy Storage Coalition (ESC) published a study showing that PJM faces an urgent near-term requirement for affordable capacity to accommodate large loads expected through 2032

The study assumes that all forecasted demand in PJM’s 2025 Load Forecast Report will materialise, which would mean that by 2028, PJM’s summer peak would increase by 16GW, and by 2032, by an additional 30GW.

Additionally, interconnection queue backlogs, long wait times for new supply, particularly gas-fired generation, and trade barriers for renewables and storage are expected to constrain PJM’s supply well into the early 2030s.

However, it is important to note that recent pushback against data centre development raises questions about whether the forecasted load will actually materialise, creating potential stranded cost risks for existing customers who could end up paying for infrastructure built to serve customers that never arrive.

“There’s a risk that data centres won’t show up, and then we have these stranded costs, and consumers might have to pay those,” Levitt acknowledges. However, he explains further, “Already the forecasts are cut by a factor of four or more relative to applications and requests. There’s many, many sites out there being developed that are not going to go through to construction, and that’s already baked into the forecast.”

If, for example, a utility builds a 1GW power plant and new transmission lines to serve a large customer, and that customer later reduces its load to 600MW or exits entirely, someone must pay for the underutilised or stranded assets. “The question is, who is going to pay for those assets?” explains Lam. “That is what we meant by the stranded cost risk.”

The reform pathways address this risk differently. Path A’s large load tariffs would require substantial upfront commitments from new customers. Path C’s approach would protect incumbent customers through long-term hedges while allowing large loads to bear more market risk.

Rate impact dynamics

Beyond the capacity market reforms, PJM’s situation highlights broader questions about how large load additions affect existing customer rates.

“If there’s enough capacity to bring these customers online, the utilities can spread the fixed system costs across more customers, thereby lowering rates for all customers, including existing customers,” Lam explains. “That is what we have observed in the last 10 years or so.”

The future trajectory depends heavily on location-specific factors. If new infrastructure costs less than the existing system average, rates may fall. If new infrastructure is more expensive, rates may rise unless costs are appropriately assigned to the new customer.

“It depends on things like whether a particular system has available capacity in order to connect these new large customers. There is no one-size-fits-all answer for all of the jurisdictions across the US,” Lam says.

For PJM specifically, the capacity constraints and need for new infrastructure suggest that careful cost allocation will be critical to protecting existing customers from rate impacts.

A silver lining for energy storage

Notably, batteries are eligible for PJM’s reliability backstop procurement.

“I actually think it’s a great opportunity for batteries, independent of this paper and independent of the energy market, just because getting into the resource adequacy procurement that has to happen beyond the capacity market is going to be super-valuable and important,” Levitt highlights.

Levitt explains that the proposed energy market reforms under the Reserve Certainty Senior Task Force (RCSTF), which was formed to address near and long-term concerns in PJM, could significantly improve the investment case for storage. These reforms would provide more precise price signals and better reflect the value of flexibility in the energy and ancillary services markets.

“If I put all that together, circumstances are driving PJM into tighter conditions, not in the capacity market, but in the energy market,” Levitt notes.

He continues, “That probably will prompt an entry signal for all kinds of resources as we get further along in the decade, and then RCSTF reforms combined with that could really promote a very substantial investment price signal for storage.”

Last summer provided a preview of this dynamic, with several days seeing prices spike over US$1,000/MWh, an hour or two prior to sundown. The RCSTF reforms would likely amplify such trends.

“It would be kind of like borrowing ERCOT’s energy-only market design and bringing it into PJM,” says Levitt.

Timeline and implementation

PJM has outlined timelines for these reforms: Path A hedging reforms could be implemented from 2026 to 2029, Path B for large new loads from 2027 to 2030, and energy market reforms for Path C from 2028 and beyond. The RCSTF reforms, which PJM says should happen regardless of which capacity market path is chosen, are targeted for 2028.

Levitt points out, “These all seem like very ambitious timelines. “I think we’re really talking about the 2030s, not 2030 but into the 2030s, realistically.”

Lam explains further, “A big focus should be on making sure that load forecasts are accurate, that the supply that is procured is actually going to be used to meet that load.” If anticipated load growth fails to materialise, existing customers could face significant cost burdens.

Though the capacity market challenges are front and centre, the energy market reforms may ultimately prove more consequential for resource investment signals, particularly for resources like BESS.

As Levitt explains of PJM’s potential reforms,”The capacity market is not meeting the present moment. It’s going to fail to procure enough capacity to meet the reliability needs.”

PJM has not committed to deciding on a path by a specific date, but it notes in the whitepaper, “The urgency is real. The supply-demand gap the region faces is substantial – it is visible in current interconnection queues, retirement notices and reserve margin forecasts. The time available to make these decisions deliberately, before operational conditions force them by default, is measured in years, not decades. PJM’s commitment is to ensure that the region uses that time well.”