UK-headquartered Zenobē Energy attracted the most venture capital (VC) funding of any company in the energy storage industry during 2023, as found by Mercom Capital.

Research group Mercom has just published its latest quarterly report into corporate funding and M&A activity in the sector. As with previous years’ fourth-quarter editions, Mercom has used its Q4 2023 report as an opportunity to offer a roundup of activity over the whole of last year.

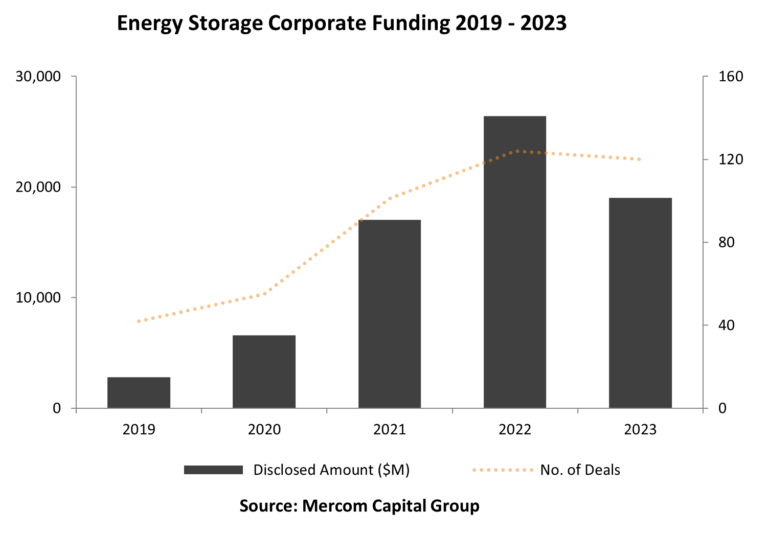

Mercom found there was a decline of 28% year-on-year (YoY) in the total sum of corporate funding, with US$19 billion raised across 120 deals in 2023, versus US$26.4 billion in 2022 from 124 deals.

It remains to be seen which will be the blip and which the trendsetter – this time last year, Mercom Capital proclaimed 2022 to have seen corporate funding at an all-time high, representing a 55% uplift from 2021’s US$17 billion total.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Analysis provided with the new report reiterated what the firm said at the time: 2022’s figures were skewed by the inclusion of LG Energy Solution’s US$10.7 billion IPO.

Conversely, VC money flowed into energy storage companies like never before in 2023. Tailwinds such as the US Inflation Reduction Act (IRA) tax credits for domestic manufacturing of clean energy technologies including batteries provided positive signals to investors, Mercom Capital CEO Raj Prabhu said.

VC funding rose 59% YoY to US$9.2 billion in 2023, across 86 deals, compared to US$5.8 billion across 96 deals the previous year. Again the dynamics make for an interesting YoY comparison, with 2021 seeing US$8.8 billion VC funding in the space. Prabhu had said the drop between 2021 and 2022 was a sign of increasing maturity in the sector.

Since then, the IRA tax credits have, as regular readers of this site will know, ushered in wave after wave of investment into US-based battery production and latterly also materials extraction and processing to feed the new gigafactories.

2023 also saw declines in the level of debt and public market financing within energy storage, as well as in the volume of M&A transactions recorded, according to Mercom.

Debt and public market financing fell 52% even though the number of deals went up, with US$9.8 billion committed through 34 deals in 2023, versus US$20.6 billion from just 28 transactions during 2022. In that year, there were 28 M&A deals, whereas in 2023, there were just 15.

While VC funding was lifted up by industry-specific tailwinds, the decline in debt and public market and M&A financings and transactions may be attributable to more general headwinds such as high interest rates, Mercom’s CEO said.

“Energy storage companies saw their highest VC funding in 2023, largely thanks to the IRA’s investment tax credit (ITC) and other incentives like manufacturing credits for battery components,” Prabhu said.

“Despite this positive trend, M&A activity lagged due to high asset valuations, elevated interest rates, and investor caution.”

Quarter-on-quarter, corporate funding into energy storage companies dropped 55% between Q3 and Q4 2023, from US$8.2 billion across 35 deals in Q3 to just US$3.7 billion from 26 deals.

VC top five list unchanged since October

Mercom also made available its ranking of the top five VC funding recipients in the sector during last year, finding it unchanged since the Q3 2023 list it put out in October last year.

Zenobē Energy, an infrastructure investor and developer in battery energy storage system (BESS) and electric fleet mobility assets based in England, UK, remained at the top of the list, having raised a total of US$1.084 billion through financing from its main existing investor, Infracapital, and US$750 million from new investor, US private equity firm KKR.

The funding was announced in September. Zenobē has already made its start on 2024 financing activities with reports this week that the developer-investor has raised £147 million towards a large-scale battery storage project in Kilmarnock, Scotland.

Coincidentally, also this week, Zenobē head of commercial products Charles Pearce appeared as a guest on Energy-Storage.news’ webinar with flexibility trader and optimiser GridBeyond, discussing Zenobē’s strategies for monetising its BESS assets on the Great Britain (GB) grid.

The session, which took place 23 January, will be available to view at the on-demand webinar section of Energy-Storage.news in the coming days.

Battery recycling and materials specialist Redwood Materials’ billion dollar Series D placed it second, with South Korea’s SK On raising US$944 million. French battery manufacturing startup Verkor, making a bid to be the first major battery producer in Southern Europe, was in fourth with US$905 million raised.

China’s Hithium, revealed to be on BloombergNEF’s inaugural Tier-1 BESS supplier list and a manufacturer of lithium batteries as well as complete BESS solutions, rounded out the top five with US$622 million raised in a Series C.

| Company | Business area | Country | Amount (US$ millions) | Funding type |

| Zenobē Energy | Developer-investor | UK | 1,084 | Undisclosed |

| Redwood Materials | Materials processing, recycling | US | 1,000 | Series D |

| SK | Battery manufacturer | South Korea | 944 | Undisclosed |

| Verkor | Battery manufacturer | France | 905 | Series C |

| Hithium | Battery and BESS manufacturer | China | 622 | Series C |

Solar PV corporate financing increased by 42%

Mercom Capital also produces quarterly reports on corporate financing in the solar PV sector, with the most recent emerging a few days before its energy storage counterpart.

Solar’s corporate financing activity went in a different direction to storage in 2023, with a 42% increase recorded versus 2022 totals. You can read coverage of that report over at our sister site PV Tech.

Energy-Storage.news’ publisher Solar Media will host the 9th annual Energy Storage Summit EU in London, 20-21 February 2024. This year it is moving to a larger venue, bringing together Europe’s leading investors, policymakers, developers, utilities, energy buyers and service providers all in one place. Visit the official site for more info.

Energy-Storage.news’ publisher Solar Media will host the 6th Energy Storage Summit USA, 19-20 March 2024 in Austin, Texas. Featuring a packed programme of panels, presentations and fireside chats from industry leaders focusing on accelerating the market for energy storage across the country. For more information, go to the website.