In 2025, BESS installations surpassed 320GWh, a y-o-y increase of over 50%. While this tells one-side of the story, the growth in cell and system shipments tells an even more significant one.

In 2025, BESS cell shipments close to doubled compared to 2024 levels, reaching over 600GWh. System shipments also saw strong growth, reaching 460GWh. The divergence between cells shipped, systems shipped, and capacity commissioned has been a hot topic in the industry over the last year and reflects the long lead times and supply chain buffers now embedded in a market expanding at pace.

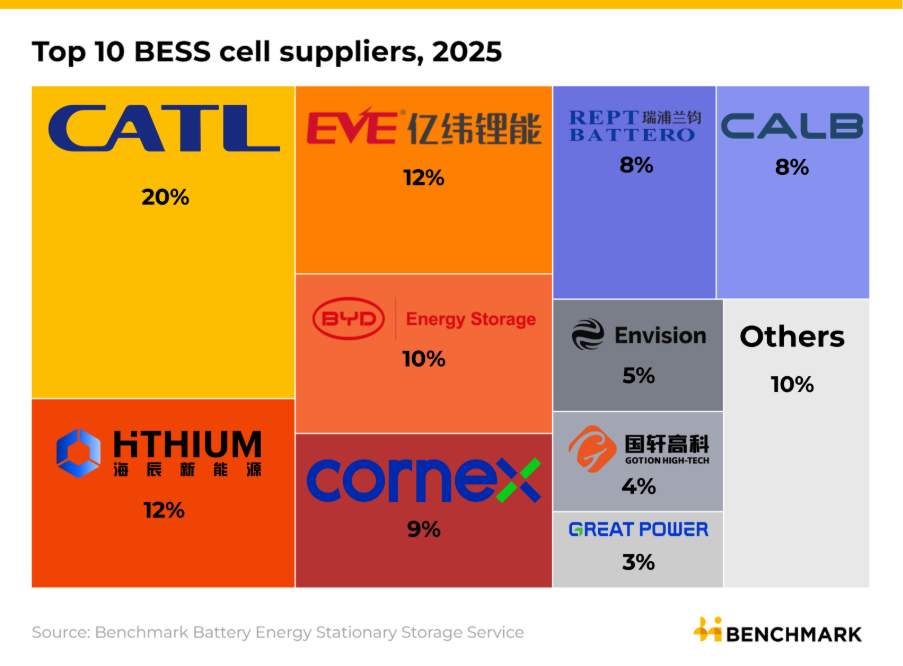

While efforts to bring LFP manufacturing outside of China are advancing, Chinese manufacturers continue to dominate, with no non-Chinese players ranked in the top 10 cell suppliers in 2025. It is worth noting that while BESS cell shipments exceeded 600GWh in 2025, nameplate capacity surpassed 1TWh for the first time by the end of the year, with over 90% of this in China. Gigafactories dedicated to or switched to BESS have grown rapidly in recent years, with nameplate capacity increasing tenfold since 2021.

CATL retained first place in global BESS cell shipments in 2025, delivering 121GWh, representing a 20% market share. Its dominance in the BESS market has continued to weaken, with its share has declined consecutively from 32% in 2023 to 29% in 2024, and now to 20%, a structural shift as competitors scale rapidly and the overall market expands faster than any single supplier can match.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

CATL in 2025 was the only cell manufacturer globally with over 100GWh of capacity dedicated to BESS. In 2026, planned expansion from EVE Energy and Hithium will see them both also surpass 100GWh of dedicated BESS capacity, with CORNEX, CALB, BYD and Great Power not far behind, each expected to exceed 70GWh of expected by year-end.

Close behind CATL, Hithium and EVE Energy each captured approximately 12% of cell shipments, taking second and third place respectively.

For Hithium, this represents a significant step up from fourth place and 9% share in 2024. The company signed a five-year, 120GWh cooperation agreement with system integrator CRRC in December 2025, underpinning continued growth.

EVE Energy, which had held second place in 2024, dropped to third but remains strongly competitive: in 2025 the company secured more than ten cell offtake agreements of at least 1GWh each, including a 50GWh deal with HyperStrong and 20GWh with Rochenergy. EVE Energy has sustained that momentum into 2026, leading offtakes YTD with over 160GWh of offtakes signed in H1 alone.

BYD, simultaneously leading the system shipment rankings, leveraged its vertically integrated position to reach a 10% share of cell shipments, placing fourth.

CORNEX, buoyed by rapid capacity expansion — over 400 GWh under construction with a further 100 GWh in the pipeline across both EV and BESS applications — broke into the top five as a late-charging contender.

The combined top ten BESS cell suppliers in 2025 accounted for over 90% of global cell shipments, and all ten are headquartered in China.

Korean manufacturers: notable by their absence

For the second year in a row, the top ten cell suppliers are all headquartered in China. Korean manufacturers, including LG Energy Solution and Samsung SDI, have fallen outside the top ten, a reflection of the Chinese dominance of LFP.

This is likely to change in the coming years, however, with significant commitments now made to BESS, in particular in the US market.

By the end of 2026, LG ES is expected to have over 50GWh of BESS cell capacity, a level that could position it to re-enter the top ten in the coming years.

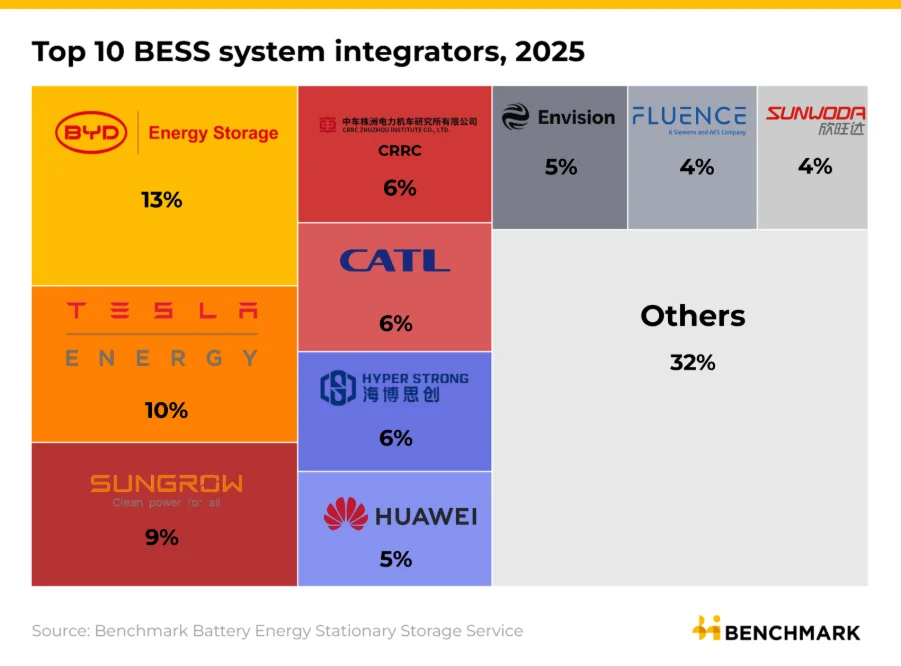

System shipments: BYD takes the crown

In 2025, around 460 GWh of BESS systems were shipped globally, with the market heavily dominated by Chinese players. Tesla and Fluence, both headquartered in the US, were the only non-Chinese companies to rank in the top ten.

BYD overtook Tesla in 2025 to claim the top spot globally, shipping 60GWh of systems and holding a 13% market share. Tesla followed with 47GWh, a 49% y-o-y increase, and Sungrow rounded out the top three with 43GWh and a 9% share. Together, the three companies accounted for roughly a third of the total systems market in 2025.

Sungrow’s storage performance was also notable for a structural reason. BESS systems became the company’s largest revenue segment in 2025, reaching 42% of total revenue and surpassing its PV inverter business, which accounted for 36%. That reversal marks a significant milestone for a company that built its global presence on inverters.

A more fragmented systems market

Unlike cells, where the top ten suppliers accounted for over 90% of volume, the system integration market is considerably more contested. The top ten system integrators collectively accounted for around 68% of shipments in 2025, with the remaining 32% split among a large number of Tier 2 and Tier 3 players, up sharply from just 18% in 2024.

That shift has been driven in part by a price war, with smaller manufacturers cutting margins to compete for market share against the dominant players. This strategy is now somewhat under pressure in 2026, with a trifecta of headwinds on the market: rising commodity price, including a significant lithium price rally, the phased removal of VAT rebates that came into force in April and will be further tightened by year-end, and the anti-involution campaign launched by the Chinese government at the end of 2025.

The competitive landscape also continues to absorb entrants from adjacent industries. Sungrow and Huawei remain the two most successful examples of solar and inverter manufacturers that pivoted early into storage systems. Huawei has climbed through its grid-forming integrated PV-storage solutions and strong residential storage performance in overseas markets.

Broader PV players – Jinko Solar, Trina Solar, and LONGi – have similarly developed storage business lines, and the trend has extended to appliance manufacturers: Haier and Gree have both established new energy divisions targeting utility-scale and C&I storage markets overseas.

Looking ahead

In 2026, BESS gigafactory capacity is set to expand further, surpassing 1.7TWh by year-end. Cell shipments are expected to approach 800 GWh, once again outpacing growth on the demand side. While time lags and inventory build account for much of this differential, the risk of overcapacity, echoing the dynamics that weighed on the EV battery market in 2024, is worth watching closely