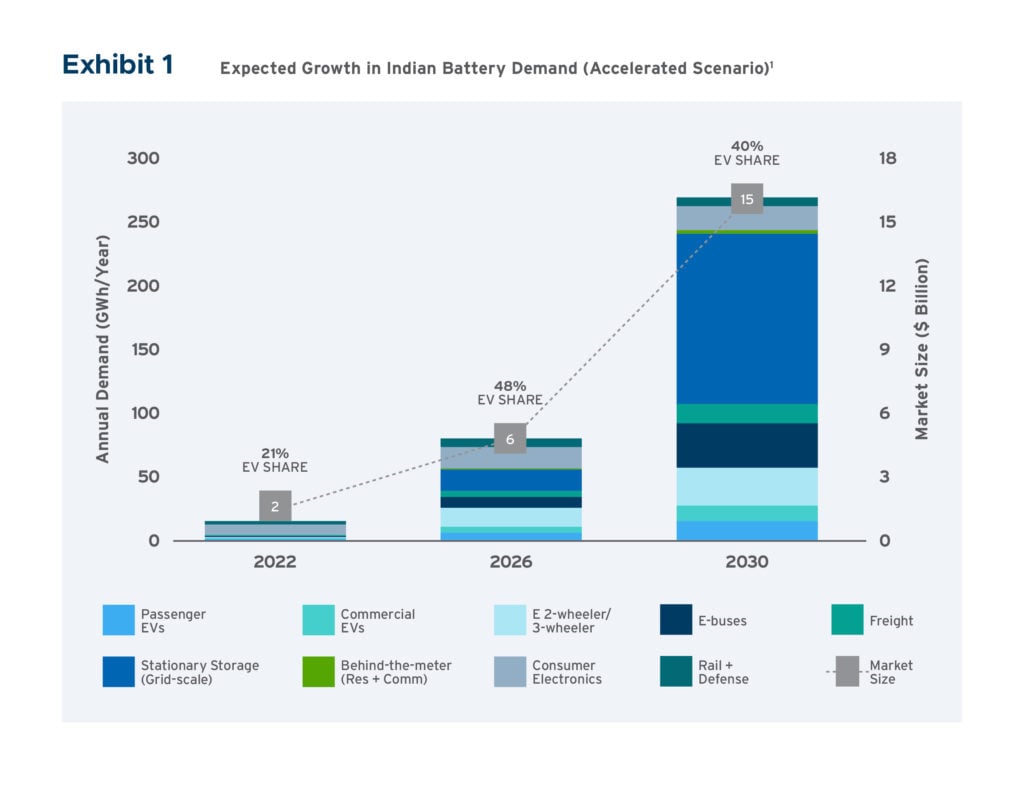

Demand for batteries in India will rise to between 106GWh and 260GWh by 2030 across sectors including transport, consumer electronics and stationary energy storage, with the country racing to build up a localised value chain.

The forecast is offered in a new report published by Indian government think tank NITI Aayog and the global and India offices of non-profit research group Rocky Mountain Institute (RMI).

It comes while a process of evaluation is underway to support the creation of 50GWh of domestic production capacity across up to 10 new facilities making so-called Advanced Chemistry Cells (ACC), through a scheme called the Production Linked Incentive (PLI).

With the nation committing over US$2 billion of financial assistance to India or overseas-headquartered companies that build cell gigafactories, each with at least 5GWh annual production capacity, the report explains the drivers behind this urgent need.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

In addition to a targeted 500GW of new renewable energy capacity to come online by 2030 — a target which the country looks on track to achieve given that it has already reached about 175GW of solar PV and wind — 30% of new vehicles sales should be electric by that time, according to Union Government policies.

Globally, the report’s authors cite BloombergNEF figures that forecast demand for energy storage at US$150 billion annually by the end of this decade. With a high penetration of EVs and stationary energy storage, India alone could represent 13% of that total demand, according to RMI and NITI Aayog.

Growth in the renewable energy market will lead naturally to a big market opportunity for stationary energy storage systems (ESS), given the wide variety of services they can provide and their declining costs mean that ESS are becoming competitive with incumbent technologies.

Broad range of value streams for broad range of stakeholders

Six major drivers are identified for the need to accelerate battery manufacturing within India:

- The centrality of batteries to taking action on climate, in line with India’s nationally determined contribution (NDC) of achieving net zero by 2070 and the meeting of 50% of energy use from non-fossil fuels by 2030.

- India currently imports not only large amounts of fossil fuels but also equipment and materials needed for renewable energy projects like solar PV modules and lithium-ion batteries. Domestic manufacturing would have a positive impact on national energy security.

- India has 22 out of the 30 most polluted cities in the world for air quality according to an IQAir index. Clean energy and electric transport offer a way to reverse this trend.

- EV adoption goals will undoubtedly drive greater demand for batteries.

- Greater involvement in battery manufacturing presents a great opportunity to grow Indian industry.

- Falling battery costs are making their use in a growing number of applications viable.

The report indexes the attractiveness of market opportunities for batteries in a range of those applications out to 2030: in stationary energy storage, grid support ancillary services, renewables integration, transmission and distribution (T&D) upgrade deferral and commercial behind-the-meter (BTM) will all be highly attractive markets by 2030.

In the case of grid services, it does depend on the ability of battery storage to be enabled by regulations to participate in wholesale markets for ancillary services, which looks increasingly likely to happen.

There are many different value streams for energy storage for India’s power grid transmission utilities and distribution companies (discoms) that can be tapped, supporting the network’s reliability and efficiency.

Energy storage can be among assets used to meet demand for electricity at peak hours of consumption, which has until now largely driven investment into peaking capacity from natural gas combustion turbines.

As is starting to be seen in other markets like the US, utilities can defer the need to invest in distribution system upgrades in areas of the grid that are seeing, or expecting to see, rapid rise in demand for electricity. Similarly, the need to make costly transmission system upgrades could be alleviated using strategically sited energy storage capacity.

Again, as seen already in many parts of the world, the direct benefit to power sector companies includes smoothing and firming renewable energy output, voltage support and frequency regulation ancillary services, black starting generation and the grid after outages or incidents and much more.

US$15 billion annual demand by 2030

According to the India Energy Storage Alliance (IESA), only around 85MWh of battery energy storage systems (BESS) are in construction or already online in the country, but there is a pipeline of 4.6GWh already (3.3GWh tendered for and 1.2GWh announced).

For the report, two scenarios were produced, one conservative, the other accelerated adoption for batteries: RMI and NITI Aayog said in the accelerated scenario (260GWh) that equates to US$15 billion of demand by 2030, US$3 billion from pack assembly and integration and US$12 billion from cells.

Even in the conservative scenario (106GWh) the annual market would be worth more than US$6 billion a year. Localising parts of the supply chain could enable the country to capture “significant value”, the report said.

It is worth noting that although electric vehicles get a lot more media attention, they will only comprise about 40% of that total demand, including freight applications, and grid-scale stationary storage will be about equal, if not more.

The report is the first of three being produced in a series, with the next two looking at aspects of directly supporting domestic production.

Part 1 of the report, ‘The Need for Advanced Chemistry Energy Storage Cells in India’ is available from RMI’s website, here.