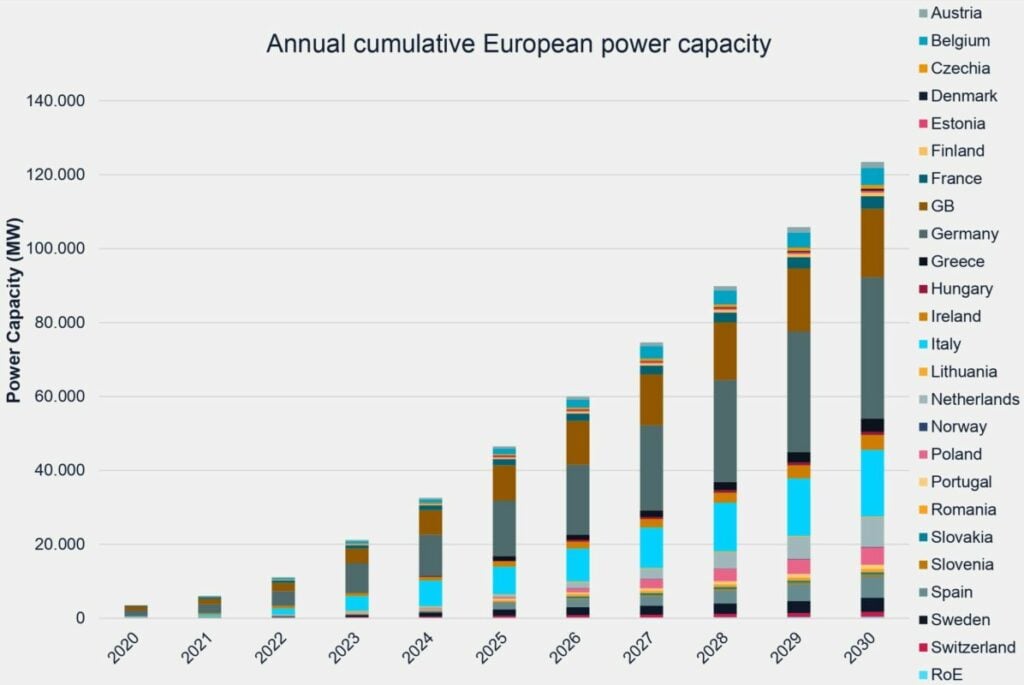

Europe has seen its first year when energy storage deployments by power capacity exceeded 10GW in 2023.

The eighth annual edition of the European Market Monitor on Energy Storage (EMMES) was published last week by consultancy LCP Delta and the European Association for Storage of Energy (EASE).

It found that total installations in Europe – including European Union (EU) and non-EU countries – across the residential, utility-scale, and commercial and industrial (C&I) market segments throughout last year added up to around 10.1GW.

That was more than double the 4.5GW recorded across Europe for 2022, and way above the 6GW forecast for 2023 by LCP Delta in last year’s EMMES 7.0 report published around this time last year.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The “impressive results” were driven by a combination of support schemes and improving market conditions for storage, LCP Delta said.

One key takeaway, which we wrote about in the most recent ESN Premium Friday Briefing, was the split between front-of-the-meter (FTM, utility-scale) and behind-the-meter (BTM, residential and C&I). There were around 2.7GW of FTM installations completed in 2023, versus around 7.3GW of BTM systems installed.

Over 500,000 residential systems deployed in Germany last year

In a webinar held earlier this month to preview and discuss the results, LCP Delta analyst Silvestros Vlachopoulos said that the BTM figure was 2.5x higher than the 2.7GW total that had been forecast a year previously.

The analysis “missed the mark by far,” Vlachopoulos said, because there was an underestimation of demand in the two leading markets in Europe for residential storage systems: Italy and Germany.

In Italy, a ‘Superbonus’ subsidy scheme for energy technologies including energy storage and renewable heat is being phased out and lower rates were paid out in 2023. While LCP Delta had thought this meant the high demand period was over, consumers’ appetite for batteries, typically paired with home solar PV systems, persisted.

Meanwhile in Germany, demand has been high for some time, particularly following the Russian invasion of Ukraine, and higher energy prices coupled with energy security fears. However, in 2022, the supply chain was constricted and storage systems couldn’t be sold and deployed fast enough to meet demand due to low stock availability.

That situation has eased up more than anticipated, “stock availability grew and was able to meet market demand,” and German households installed more than 500,000 residential battery systems in the past year.

Residential dominated the BTM segment, and another dynamic was that average system sizes across Europe continued to grow.

In the front-of-the-meter segment, LCP Delta’s forecast was conversely higher than the final tally, although with much less disparity than in the residential estimation.

Projects forecast to come online in 2023 experienced delays due to factors including grid connection waiting times as well as regulatory and policy uncertainty, while around half of a 1.7GW portfolio being built by Enel in Italy was expected to go into commercial operation last year but has been pushed back – albeit those projects are still going ahead and expected to be completed soon, the analyst said.

The next year or two will see much-improved prospects for FTM storage in selected markets, with Italy again a standout, due to grid operator TERNA forecasting a need for 8GW/70GWh of deployments by 2030 and targeting the procurement of a portion of that sum through the forthcoming MACSE capacity market tenders.

“A lot of capacity” will be unlocked in the Netherlands in the medium-term through improving market conditions, while Belgium and Poland’s capacity market auctions will drive deployments towards the end of this decade.

The storage durations of utility-scale FTM projects in Europe is expected to “grow very fast, very soon,” Vlachopoulos said, with roughly 1.5-hours the average duration for >10MW projects deployed in 2023. There are increasing numbers of 2-hour duration projects being built, while development pipelines in “multiple countries” include 4-hour projects.

‘Mismatch’ in Europe between deployment speed and need for storage

Jacopo Topsoni, head of policy at EASE, said that there is growing recognition at both EU level and at national level that there is a mismatch between deployment rates in Member States and the amount of storage that will be required to meet EU goals on renewables and electricity system flexibility.

National policymakers in the EU will have “several tools at their disposal” to address this mismatch. These include making regulatory changes to remove barriers to storage deployment, introducing or reforming capacity market mechanisms, introducing national targets or strategies, and introducing support schemes and storage-specific auctions.

Topsoni noted a “shift in policy trends,” had occurred in 2023, from national policymakers in Europe being focused previously on setting basic frameworks for increased market participation of storage, by adding new revenue streams and opening up markets to aggregation and other business models.

This has again shifted, and in short, there is “recognition there needs to be more deployment,” Topsoni said, noting that there will be more grid services products rolled out, removals of tariffs and grid fees, and more favourable tax conditions in general.

There is also the Electricity Market Design (EMD) reform process, which is ongoing, and Topsoni said that both the European Commission and pan-European regulator ACER have been “vocal” about removing barriers to storage deployment through this process.

While still a work in progress, EMD will introduce requirements for Member States of the EU to make regular flexibility assessments of their electricity grids, which will in effect mean they must also create targets for energy storage, which is a key tool to add that flexibility. EU nations can then introduce support schemes to get to those targets.

This is very different from the current situation, where only a handful of states, such as Spain and Italy, have introduced strategies or targets around storage. Germany is another which is presently formulating its own strategy.

However, while Member States will be mandated to reach those national flexibility objectives, they will not be introduced until 2027. While countries are free to go faster than mandated, it seems likely EMD will not present a significant boost to deployments until the latter part of this decade, Topsoni said.

The EASE policy director also said that creating a methodology for assessing flexibility needs will be challenging, and that it is essential the association of grid operators, ENTSO-E, and regulator ACER, get that part right.