Wood Mackenzie has forecast that the US energy storage industry will install around half a terawatt-hour of new capacity over the next five years.

The market analysis group has just published the newest edition of its US Energy Storage Monitor quarterly report, in partnership with the American Clean Power Association (ACP).

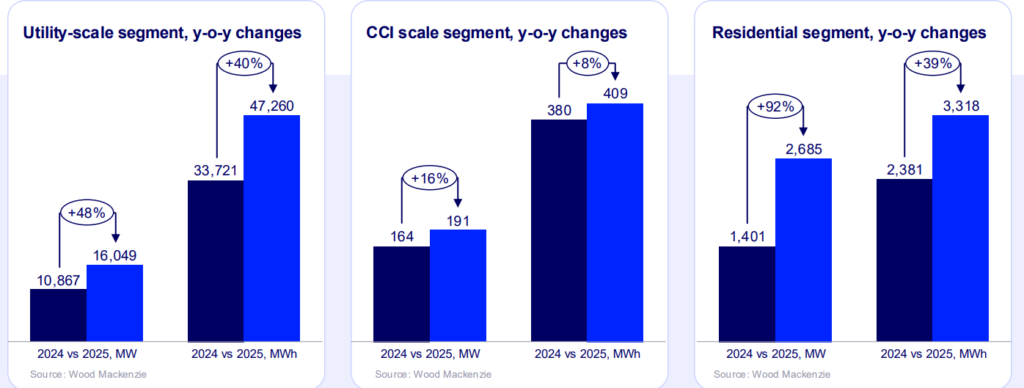

The Q1 2026 report offers full 2025 data as well as numbers for Q4 2025. Both full-year and latest quarterly totals were the highest on record to date: 18.9GW/51GWh of battery energy storage system (BESS) projects across utility-scale, residential and community, commercial and industrial segments were deployed throughout the year.

By comparison, Wood Mackenzie had found around this time last year that just over 12GW/37GWh was installed in 2024, around 9.3GW/27.7GWh in 2023 and about 4.8GW/13.2GWh in 2022. 2024 had been the first year in which gigawatt deployment figures went into the double-digit range.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Meanwhile the biggest quarter on record saw 5.8GW of installations by power and 14.8GWh in energy storage capacity, with 4.9GW in the utility-scale segment of the market, according to Wood Mackenzie. In Q4 2024, the firm had reported 3.3GW of installs, with the final quarter of last year marking a considerable year-over-year jump.

As indicated by the above, the rapidly growing US market has seen records broken frequently. Last year’s installations had already surpassed 2024’s by the time the Q4 2025 edition of the US Energy Storage Monitor was released in December, finding a total of 12.6GW of new storage deployed during the year by the end of Q3 2025.

OBBBA and FEOC brought uncertainty to market in 2025

Speaking with ESN Premium last month at this year’s Energy Storage Summit in the UK, Wood Mackenzie’s global head of energy storage research, Alisson Weiss, said that despite regulatory and policy changes in the US which had brought uncertainty to the market, the market had remained strong largely because energy storage retained the investment tax credit (ITC) that had been stripped away from solar PV and wind.

Other drivers of the record 2025 numbers included low system costs and growing interest in offtake by US utility companies, while the market saw continuing regional diversification: including the two long-established leading markets by state of California and Texas, Wood Mackenzie tracked new projects in 13 US states, two more than in the previous edition of the report.

Tax incentives also drove record performance in the residential segment, albeit in a less positive manner. Last year, 2.7GW of residential installs were completed, a 92% increase from 2024, and this was due in no small part to the phasing out of the ITC for purchased residential systems.

The community, commercial and industrial segment, often abbreviated to commercial and industrial (C&I), remains the laggard despite 16% year-on-year growth from 2024, registering just 95.6MW in 2025. The vast majority of that, 77MW, was installed in Q4.

In our February interview, published in two parts as a comparison piece between US and European market dynamics and with the co-participation of Wood Mackenzie EMEA energy storage analyst Anna Darmani, Allison Weiss had said that the record-breaking streak is likely to end this year.

“We see less storage coming online this year in 2026 than we had in 2025,” Weiss said.

“A lot of that is just that things did not get signed when tariffs were bouncing around, and then we had the ‘One, Big, Beautiful Bill Act’ (‘OBBA’) passed, and so people had to move very quickly to try to get stuff safe harboured before the Foreign Entity of Concern (FEOC) restrictions went in place.”

FEOC restrictions, introduced with the OBBA legislation and in effect since 1 January 2026, disqualify energy storage projects from the ITC incentives if their developers and owners receive significant aid from companies based in FEOC nations, including China, the world’s main exporter of battery products, materials and components.

500GWh prediction, big gap between high and low scenarios

However, the market research firm has since withdrawn its expectation of a near-term market contraction, because a record number of projects began construction in late 2025 to lock in the ITC, making up for a shortfall as activity slowed down mid-year.

Therefore, even accounting for those challenges and new findings that utility-scale battery system prices went up 23% year-on-year from 2024 to 2025, Wood Mackenzie expects the US market to retain momentum. That momentum to date has led to more than 50GW and 144GWh of installs between 2019 and 2025.

Wood Mackenzie has forecasted that between 2026 and 2031, around 500GWh of battery storage will be deployed, which would be 22.5x what was installed in the years 2025-2030.

The firm has established Low, Base and High scenarios for its market expectations. It predicts that annual installations could surpass 36GW in 2031 under the High scenario in which policy changes are minimal and developers navigate their way through US Treasury guidance on FEOC rules smoothly, while state level policies remain supportive.

However, if the market more closely resembles the Base scenario in which FEOC guidance limits short-term procurement but is more workable long-term, US-China import tariffs remain at similar rates and there is a “slight thaw” in the Federal freeze on permitting projects on public land, it could be closer to 28GW.

In the meantime, in a Low scenario market, restricted by FEOC guidance that constrains battery cell availability and increasingly protectionist import-export policies, among other drivers, the swing downwards could be much greater, according to Wood Mackenzie.