The UK’s energy retail market is witnessing an exodus of customers leaving the so-called Big Six for independent suppliers, who are attracting them with home solar systems and a battery to match. Liam Stoker uncovers what’s behind the trend for new energy suppliers taking to domestic PV. This article first appeared in ‘Storage & Smart Power’, Energy-Storage.news’ dedicated section in Solar Media’s quarterly journal PV Tech Power, vol.19.

The UK’s energy retail market is, slowly but surely, changing beyond recognition. Ever since the market was privatised in 1990, it has been dominated by a select handful of companies whose combined share of the market has at times topped 99%.

Now, nearly 30 years later, that status is changing and their footing is being eroded by an influx of independent operators with a stated aim of giving power back to the people. Increasingly, they are turning to solar and storage to do that.

The heavy hitters of the UK retail market, dubbed The Big Six, are British Gas (parent: Centrica), E.On, EDF Energy, npower (parent: innogy/RWE), ScottishPower (parent: Iberdrola) and SSE. Although historically they have enjoyed an oligopoly over UK homes, a government-backed drive to encourage switching, political uproar over increasing bills and heightened consumer engagement with their energy supply has turned the market on its head.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Ofgem, the UK energy regulator, charts the market share of all suppliers over a certain threshold and its most recent dataset, for Q3 2018, places the collective Big Six market share at 75%, indicating the sheer level at which consumers have started to vote with their feet. Solar and storage systems, so adept at handing power back to the people, are causing a shift in market share towards independent suppliers.

Empowering software

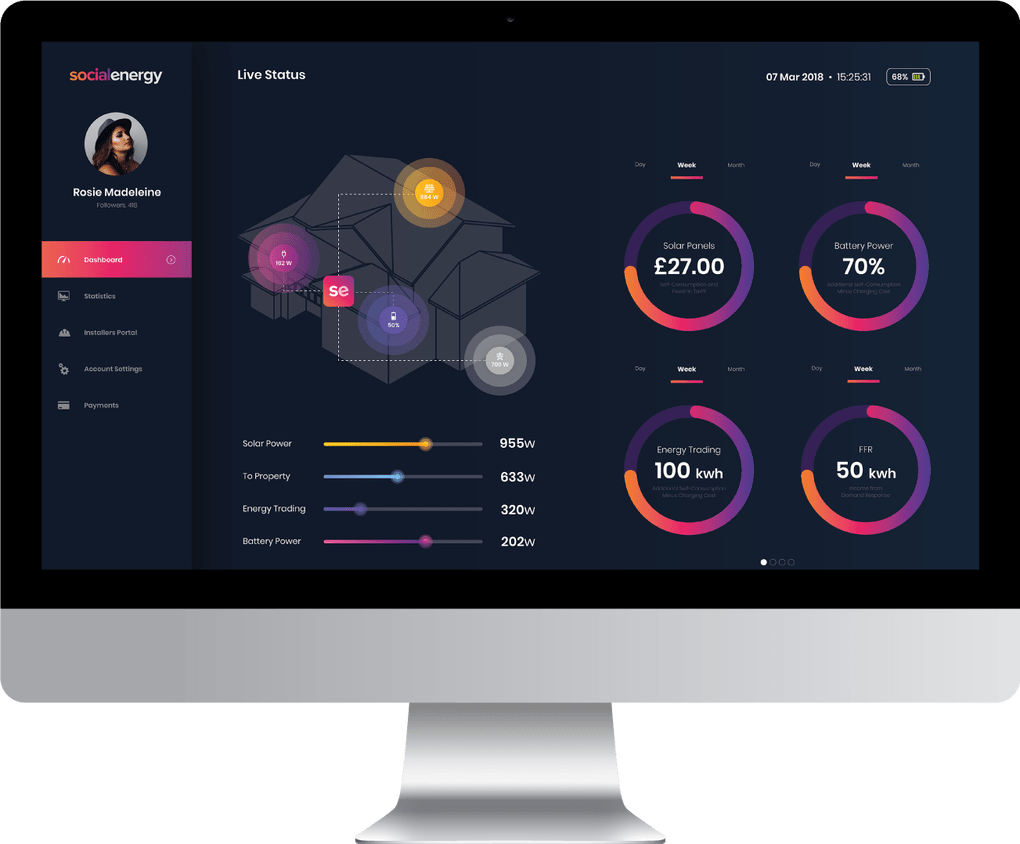

Social Energy, one such independent new entrant, launched with much fanfare earlier this year. While technically an energy supplier – it holds a supply licence – its chief executive Ryan Gill describes the company as “more Microsoft than Apple” by the way it has developed bespoke software which is then added to third-party equipment.

And it’s that software which has enabled Social Energy to lay claim to kick-starting a revolution in home solar in the UK.

It uses artificial intelligence techniques to educate an algorithm which effectively assesses and manages individual home solar and storage systems every five minutes, meaning the company engages with its customer more than 100,000 times each year. To put that figure into context, during a recent trial of its system with National Grid to qualify it to be used in grid balancing services, Gill says the company delivered 11.2 billion pieces of data to the system operator.

Gill says this level of engagement allows the company to radically enhance the effectiveness of the systems it manages, taking them into revenue streams and balancing markets which are uncharted territory for domestic solar. Homes will be capable of providing their flexibility into frequency response markets, with ambitions to enter the Capacity and Balancing Markets in the future. Social’s supply licence also allows homes to subvert network charges at times they are most costly. When combined with more standard self- consumption and spot trading benefits, batteries featuring Social’s software are almost supercharged.

“What this allows us to do is deliver a return on investment that’s actually better than solar tariffs at their peak,” Gill says, referring to the UK’s feed-in tariff which, once upon a time, stood at a richly rewarding 43.3p/kWh (US$0.55/kWh). At that time a standard 4kW system returned an ROI figure of around 348%. Social’s heady mix of revenue streams, certainly aided by cost reductions which place a standard 4kW PV system plus 4kWh battery at circa £8,500, means that Social boasts a ROI figure of 365%.

Put bluntly, Social Energy’s combination of self-generation and storage benefits professes to render solar and storage systems so economical they’d essentially pay for themselves significantly quicker than they could otherwise. But they’re not alone. Another independent supplier, Resilience Energy, caught attention earlier this year with a similar model and the bold intention of establishing itself as the “Uber of Electricity” and “future proofing” homes with energy saving – and generating – technologies.

Loic Hares, founder and chief executive at Resilience, says the company’s bespoke platform would not only trade surplus power more efficiently and provide flexibility services to network operators, but allow Resilience to autonomously predict when system faults are likely to occur. Both models are reflective of a growing trend in global power markets, with ‘prosumers’ replacing consumers. Hares says this is particularly true in a UK sector where the public has grown frustrated with years of neglect.

The virtual challenge

Another such challenge could emerge from a range of projects unveiled by the UK government in early April, combining not just solar and storage but a raft of other smart technologies to deliver tangible benefits to consumers.

One of those, dubbed the Smart Local Energy System (SLES) project on the UK’s south coast, is to effectively link solar panels, batteries and electric vehicles across hundreds of homes, schools and council buildings – alongside a marine source heat pump, a grid-scale battery and a hybrid, electric/hydrogen fuel cell vehicle refuelling station – throughout West Sussex.

Moixa, the British battery storage company currently making waves in Japan, is to incorporate the technologies into a virtual power plant (VPP), which the firm’s chief technology officer Chris Wright says will demonstrate the benefits of linking power, heat and transport in one local system.

The three-year pilot scheme is expected to cut energy costs by around 10% per user. With Ofgem placing the average UK dual-fuel energy bill at around £1,150 per year, combining solar and other technologies to save consumers more than £100 could be a winning formula. Moixa and its project partners are also backing the combination to hold the potential to save the UK some £32 billion on infrastructure spending by 2035 – harnessing more flexible power will reduce the need for costly network upgrades – which will again, in turn, come off the bills of consumers.

Ultimately, Moixa intends to install about 4MW of generation and 4.2MWh of battery storage, which is to be combined with other technologies to result in just over 7MW of generation and 17MWh of storage, all of which will be managed by Flexitricity. But perhaps the biggest challenger to the Big Six’s status will arise from a common household name not usually associated with renewables.

Shelling out

In 2018, O&G major Shell completed its acquisition of First Utility, a supplier sitting just outside the ranks of the Big Six with around 700,000 customers nationwide. Aside from positioning First Utility firmly within its New Energies unit, Shell remained coy on what, exactly, it wanted to do with the purchase. Until earlier this year.

In late March Shell tied its billion-dollar brand to the UK energy retail market by rebranding First Utility as Shell Energy and switching all of its customers to a renewables-only tariff overnight, at no extra cost. It also combined energy supply with broadband internet services – the kind of utility bundling many in the energy retail sector hope to accelerate rapidly in the coming years – and, crucially, introduce new domestic energy technologies to its offering.

Customers of Shell Energy receive discounted smart thermostats supplied by Nest and can pick up a domestic EV charger from NewMotion, the Dutch manufacturer Shell acquired in October 2017. That ability to dip into companies acquired and siloed within its New Energies division would become all the more relevant just a day later.

Colin Crooks, chief executive at Shell Energy, took to the stage at an industry event in London just over 24 hours later and detailed his company’s strategy for tackling the Big Six’s stranglehold on energy supply. Referring to the rebrand as a “line in the sand, a statement of intent” for Shell, he revealed that the company would indeed also be introducing sonnen batteries to customers imminently, leveraging the German battery storage manufacturer it acquired just a few months before.

Crooks described sonnen’s offering as “the best home battery storage solution in the world” in what constitutes a fairly significant shot across the bows of Tesla et al. But the home battery itself may only be part of the solution. Crooks went on to discuss how other facets of Shell New Energies – London-based virtual power plant specialist Limejump, which it too acquired earlier this year, and billing app Wonderbill – could combine to create a supply revolution.

“What’s exciting about this is that each part of the story is actually working somewhere in the world. We haven’t had to invent it all from scratch… but while much of the world does some of this well, nowhere is pulling it all together.

“And that’s the opportunity we see today, to find the best people, to invest in the best technologies and bring them together in ways which empower and excite our customers,” Crooks said.

Shell’s decision to place consumer-facing technologies such as battery storage firmly within their offering is down, Crooks adds, to a need to induce “enormous levels of investment and profound changes in consumer behaviour” in order to both transition away from fossil fuels and engage consumers with their energy supply.

It’s something which sonnen chief executive Christoph Ostermann is also a huge advocate of. Speaking to Energy-Storage.News after his firm’s acquisition was finalised, he said: “The equipment we provide is a solution for residential customers. A customer can supply themselves with self-generated solar power on the one hand, on the other hand, in the bundle with First Utility, First Utility could provide that customer with the remaining grid power that they still need. The customer could buy this as a package. It’s a very nice opportunity to offer more complete packages to the residential customer.”

Combining sonnen’s product suite – the manufacturer’s sonnencommunity virtual power plant has already been tried and tested in the UK – with Shell’s 700,000-strong customer base could make for a potent mix, especially when you factor in the obvious synergies in introducing the aggregated capacity of those batteries, some of which could be coupled with solar, into grid balancing markets using Limejump’s capabilities.

But as Crooks says, cracking the market will either require a sea change in consumer behaviour or an easier, more penetrative way for batteries to become more prevalent in consumer homes. Enter the electric vehicle.

Driving change

The electrification of transport, specifically the personal vehicle, is driving car companies into the energy market at speed. Automotive giants have quickly come around to the concept that they will soon be purveyors of batteries on wheels, embracing the change that comes with it. As has been identified by Moixa, the average electric vehicle’s battery is six-times the size of its domestic counterpart at ~30kWh, making them an ideal resource to pull from. This proved to be a significant contributing factor to Honda saddling up to Moixa earlier this year in a partnership designed to strengthen the duo’s collaboration in the energy sphere moving forward.

This, too, is forcing them to at least consider bolting on additional services. Last year Nissan partnered with UK PV firm Solarcentury to launch a domestic solar-plus-storage offering, making full use of the second-life battery partnership it has with Eaton, while earlier this year Volkswagen – perhaps still conscious of the reputational hit it suffered via ‘Dieselgate’ – announced the launch of a 100% renewable supply arm dubbed Elli. Buying an electric VW? The dealership will now be offering you a 100% green tariff to power it and a home charger install for the trouble.

Whether or not consumers will take to purchasing their home’s energy from a car dealership remains to be seen. Trust has proven to be a significant hurdle for UK energy suppliers and, if anything, trust in car manufacturers is low post-Dieselgate. The same could be said for Shell and its renewable credentials, after its announcement was pilloried by eco groups in the UK. But independents will face hurdles too as they attempt to get their fledgling models off the ground.

Trading places

Such is the pace of change within the UK’s energy sector that fears remain that decentralised energy may be attempting to run before it can walk. When the UK government consulted on proposals for a replacement scheme for its feed-in tariffs for solar, the UK’s Solar Trade Association raised a multitude of concerns on its reliance on technologies which just aren’t ready for at-scale deployment. Smart meters, for example, are a technology crucial to everything working in tandem, but installations are considerably behind schedule.

One energy company questioned for this piece also raised serious concerns over using such systems to bid into flexibility markets and factoring these revenue streams into the economics of individual installations, suggesting that would-be installers could end up over-promising and under-delivering.

UK grid balancing markets are plentiful, but complicated. Entry barriers are high and often participating in one precludes you from opportunities in another, allowing network operators to guarantee that flexibility is available should they need to call on it. This extends into the battery’s operation, meaning that if a VPP operator or aggregator has secured a contract, as long as it is participating in that market it cannot be utilised by its actual owner. “Try explaining to a customer they can’t use their battery or car because their energy supplier is using it instead,” the energy company representative said.

There are apparent workarounds. Moixa, for instance is only taking surplus capacity into flexibility markets to bolster its project economics and Social Energy packages homes in groups of 400 for flexibility provision, rather than the minimum necessary 330, to account for any connectivity issues or instances where devices are already in use.

Concerns over the financial benefits attached to flexibility markets have too been raised, particularly as competition for such payments stands to increase. Social’s model has been backed by energy consultancy Baringa, lending it a considerable amount of authority in the market, but industry scepticism looks only set to continue until such a time that installs are demonstrably achieving what they’ve set out to.

Any apprehension would not appear to have extended as far as the consumer, however. Gill says Social Energy is preparing to install as many 1,000 domestic batteries per month by the summer, with a target of installing twice or three-times as many per month by the end of this year. Its software will soon be approved to be used in conjunction with a number of new batteries from an extended range of manufacturers, and the company has turned to renowned investment advisory Evercore to raise £90 million to fund an expansion into Australia, the US and, like Moixa before them, Japan, where the market for intelligent battery systems has exploded.

Fears of running before these systems can walk could be well founded, but there is most certainly appetite for solar and storage to be installed en masse and, although the likes of E.On and EDF have their own established offerings, the exodus of consumers from the Big Six is changing the face of the UK’s energy retail market for good.

Intelligent solar and storage could prove to be the accelerant needed.

This article has just appeared in PV Tech Power Vol.19, Solar Media’s quarterly tech journal for the downstream global PV industry, as part of ‘Storage & Smart Power’, a dedicated section commissioned and brought to you by the team here at Energy-Storage.news. Download the whole 119-page magazine for free, here (subscription required).

Cover image: Shell rebranded its First Utility supply business as Shell Energy in March 2019, before promising to offer its 700,000 customers battery storage. Credit: Shell Energy.